Table of Contents

- Introduction

- The Harsh Truth: Why Saving Feels Impossible

- 1. Lack of a Clear Goal

- 2. Living Paycheck to Paycheck

- 3. No Budgeting System

- 4. Lifestyle Inflation

- 5. Emotional Spending Habits

- 6. Debt Trap and Minimum Payments

- How to Finally Succeed at Saving

- Step-by-Step: Build a Savings System That Sticks

- Real-Life Example: The $100-a-Month Rule

- Free Tools to Track and Grow Your Savings

- Conclusion

- FAQs

Introduction

If you’ve ever promised yourself to “start saving next month,” only to end up wondering where your paycheck went—welcome to the club.

According to the Federal Reserve, nearly 36% of Americans can’t cover a $400 emergency expense without borrowing or selling something.

Saving isn’t just about math—it’s about behavior, psychology, and systems.

In this guide, we’ll uncover why most people fail to save money, and more importantly, how you can succeed using simple, proven strategies that anyone can apply starting today.

The Harsh Truth: Why Saving Feels Impossible

Saving money often feels like trying to fill a bucket with a hole in it.

Every time you make progress, something unexpected drains your balance—car repair, medical bill, or “just one more thing” from Amazon.

But here’s the truth: you don’t fail to save because you’re bad with money—you fail because the system you use is broken.

Let’s break down the most common reasons behind this.

1. Lack of a Clear Goal

You can’t hit a target you can’t see.

Most people start saving with vague intentions like “I’ll try to save more,” but without a defined purpose, it’s easy to quit.

🎯 Action Step: Name your savings goal.

Examples: “Emergency fund of $1,000,” “Down payment for a car,” or “3-month safety net.”When your savings have meaning, every dollar feels like progress toward something real.

2. Living Paycheck to Paycheck

Even high-income earners fall into this trap.

A CNBC survey (2024) found that over 60% of Americans earning six figures live paycheck to paycheck.

Why? Because expenses rise with income.

You get a raise → upgrade your lifestyle → no real gain in savings.

💡 Expert Insight (Backlinko-style):

Financial success isn’t about what you earn—it’s about what you keep consistently.

3. No Budgeting System

If your money management plan is “check the bank app sometimes,” you don’t have a plan—you have stress.

Budgeting isn’t restrictive; it’s empowering.

Three proven methods:

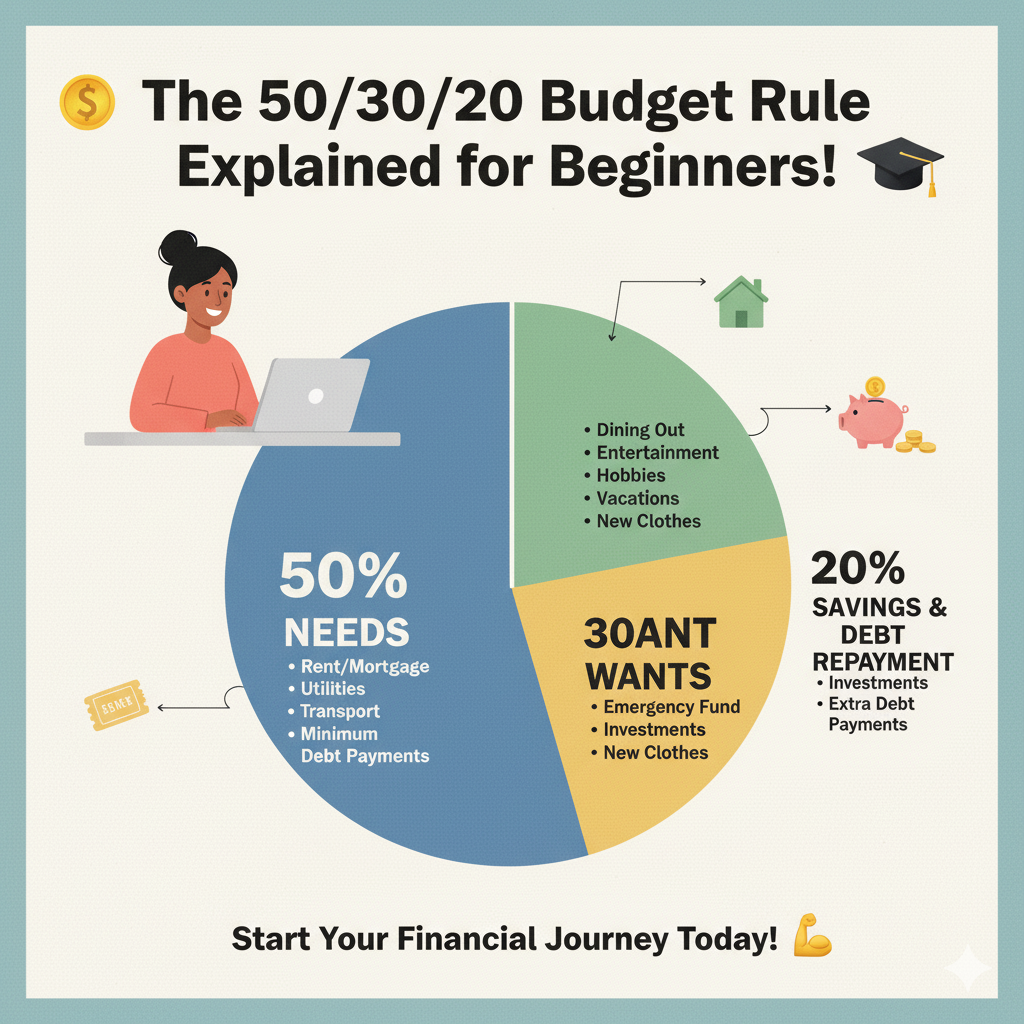

- 50/30/20 Rule – 50% needs, 30% wants, 20% savings.

- Zero-Based Budgeting – Every dollar gets a job.

- Pay-Yourself-First – Save before you spend, not after.

🧾 Pro Tip: Use a simple spreadsheet or Google Sheets template.

(Internal link placeholder: See our free budgeting template here)

4. Lifestyle Inflation

Lifestyle inflation happens when spending grows as income grows.

New job? New car. Bigger paycheck? Bigger rent.

You don’t feel richer because your expenses expand to match your earnings.

🚫 Fix: Lock in your lifestyle for one year after a raise.

Use new income to build savings or investments instead.

5. Emotional Spending Habits

Money decisions are emotional—more than logical.

You buy a latte because it feels good, not because you need it.

Common emotional triggers:

- Stress → impulse shopping

- Boredom → online browsing

- Comparison → keeping up with others

🧠 Mindset Shift: Before any non-essential purchase, ask:

“Will this make me happier next week—or just right now?”

6. Debt Trap and Minimum Payments

Debt isn’t just a financial problem—it’s a savings killer.

High-interest credit card debt (often 20–25% APR) eats away what you could have saved.

📉 Example:

$5,000 in credit card debt at 22% APR costs $1,100+ per year in interest.

That’s money that could’ve built your emergency fund.

✅ Solution:

Focus on the Debt Avalanche method—pay off the highest-interest debt first while making minimums on the rest.

How to Finally Succeed at Saving

To succeed at saving, you need a system, not just willpower.

Here’s what the pros do differently:

- Automate savings – Treat savings like a bill you must pay.

- Track progress visually – See your growth to stay motivated.

- Use psychology to your advantage – Start small, build consistency.

- Keep savings hard to access – Out of sight = out of mind.

💬 “If saving feels easy, you’ve built the right system.”

Step-by-Step: Build a Savings System That Sticks

Step 1: Calculate Your True Monthly Expenses

List your fixed (rent, bills, insurance) and variable (food, gas, fun) expenses.

Average the last 3 months for accuracy.

Step 2: Set a Realistic Savings Goal

Start small — $100 a month is a win if it’s consistent.

Gradually raise it as you eliminate unnecessary spending.

Step 3: Automate Transfers

Set up an auto-transfer on payday to your savings account.

Even $25 weekly builds momentum.

Step 4: Use the 50/30/20 Framework

| Category | Percentage | Example (Monthly Income: $3,000) |

|---|---|---|

| Needs | 50% | $1,500 |

| Wants | 30% | $900 |

| Savings | 20% | $600 |

Step 5: Reward Progress

Hit milestones? Celebrate (cheaply).

This positive feedback keeps you going long-term.

Real-Life Example: The $100-a-Month Rule

Let’s say Emma, a 27-year-old graphic designer, struggled to save.

She applied a simple rule: Save $100 from every paycheck automatically.

After 12 months:

- $2,400 saved

- Emergency fund established

- Less anxiety about bills

That small, automatic step created momentum—eventually increasing her savings rate to 25%.

Free Tools to Track and Grow Your Savings

You don’t need paid apps. Try these free, trusted tools:

- Google Sheets – Customizable budgeting & tracking.

- Mint – Expense categorization and visual summaries.

- Cleo (free tier) – AI-based chat budgeting (U.S.-based).

- Google Trends – Track inflation or savings topics.

- PageSpeed Insights / Search Console – If building a finance blog to share your journey.

(Internal link placeholder: See full list of recommended finance tools)

Conclusion

Most people fail to save—not because they don’t care, but because their money system doesn’t match their psychology.

Success comes when you:

- Give every dollar a purpose,

- Automate your savings, and

- Focus on consistent progress, not perfection.

Start today, even if it’s just $10 a week.

Because in personal finance, small wins compound into life-changing results.

🏁 Call to Action:

Take 10 minutes today to set up your first automatic transfer.

Next month, you’ll thank yourself.

FAQs

1. Why is saving money so hard?

Because humans are wired for short-term gratification. The fix: automate savings so it happens before temptation.

2. How much should I save each month?

Aim for at least 20% of your income, but start smaller if needed. Consistency matters more than amount.

3. What’s the first step if I’m in debt?

Build a mini-emergency fund ($500–$1,000), then focus on high-interest debt using the Avalanche method.

4. Should I invest or save first?

Always save a 3-month emergency fund before investing. It gives you peace and stability.

5. What if I live paycheck to paycheck?

Track every dollar for 30 days. You’ll uncover at least one area to cut and redirect toward savings.